Oil Just Hit $90: What the Iran Crisis Means for Energy Stocks and Commodity ETFs

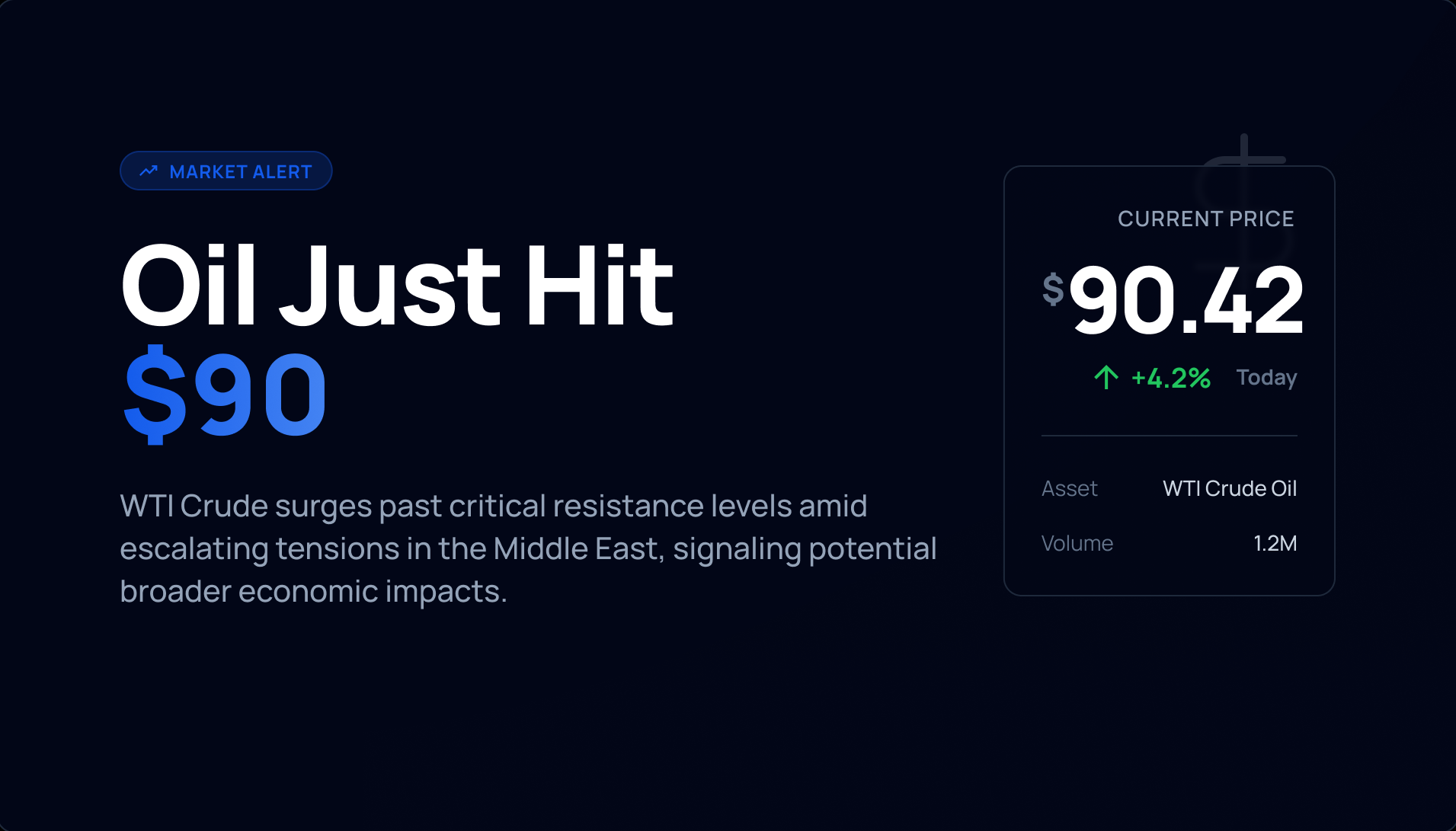

WTI crude oil crossed $90 per barrel this week — up 35% in five days. Brent surged 28%. If you’ve been watching the news, you already know why: the United States and Israel launched coordinated strikes on Iran on February 28th, and Iran retaliated by threatening the Strait of Hormuz, the narrow waterway through which roughly 20% of the world’s oil supply passes every day.

What happened next wasn’t a military blockade — it was an insurance shutdown. After Iran conducted drone strikes near the strait, insurers pulled coverage for tankers transiting the area. No insurance means no shipping. Tanker traffic dropped by 70% almost overnight, then fell to near zero. Over 150 ships sat anchored outside the strait, waiting. The result: the biggest supply disruption since the 1970s oil embargo.

Energy stocks have responded. XLE, the energy sector ETF, is up over 22% year-to-date. Our top-scored energy stocks — MPC, OKE, COP, EOG — are all posting strong gains. Commodity ETFs tracking oil and broad baskets have spiked too.

But here’s the question every investor should be asking right now: is this the moment to buy energy, or is this the moment you’ll regret buying?

The answer depends entirely on how you get exposure and why. Let’s break it down.

Three Ways to Play Oil

Not all oil exposure is created equal. There are three fundamentally different approaches, and choosing the wrong one can cost you — even if you’re right about oil prices going up.

1. Energy Stocks

Companies like XOM, CVX, COP, and EOG produce, refine, or transport oil. When you buy their shares, you own a business — one that generates revenue, pays dividends, and (ideally) grows over time. Our scoring system evaluates them across four pillars: shareholder returns, growth quality, valuation quality, and track record.

Energy stocks don’t track oil prices 1:1. A well-managed company like EOG can outperform crude oil itself through disciplined capital allocation and low-cost production. A poorly-run company can lag even when oil is booming. That’s the whole point — you’re betting on the business, not just the commodity.

Pros: Dividends, real earnings, manageable with fundamental analysis, no contango drag. Cons: Company-specific risk, won’t capture 100% of an oil price move.

2. Oil ETFs (Direct Futures Exposure)

USO tracks WTI crude futures. BNO tracks Brent. These give you the most direct exposure to oil prices — but they come with a hidden cost that destroys long-term returns.

It’s called contango, and it works like this: if oil is $90 today but next month’s futures contract is priced at $92, USO has to sell the expiring $90 contract and buy the $92 one. You just lost $2 per barrel in value — not because oil went down, but because of the mechanics of rolling futures contracts. Over months and years, this “roll cost” compounds brutally. USO has destroyed long-term holders even during periods when oil prices recovered.

Pros: Closest to tracking spot oil price daily. Cons: Contango erodes returns over time, issues K-1 tax forms, terrible for buy-and-hold.

3. Broad Commodity ETFs

DBC, GSG, and PDBC hold baskets of commodity futures — oil, natural gas, metals, agriculture. They’re more diversified than pure oil ETFs and serve as inflation hedges. The key difference between them is taxes: DBC and GSG issue K-1 forms (a tax headache), while PDBC issues a standard 1099.

These work well as a small allocation in a diversified portfolio — like the 7.5% commodity slice in the All Weather portfolio — but they won’t capture the full oil spike because oil is only one component of the basket.

Pros: Diversified commodity exposure, inflation hedge. Cons: Still futures-based (contango applies), diluted oil exposure.

Our Take

For most investors, energy stocks are the best way to play oil long-term. You get dividends, real business fundamentals, and our scoring system can help you pick the best ones. Use broad commodity ETFs like PDBC for portfolio diversification, not as an oil bet. And avoid pure oil futures ETFs like USO unless you’re a short-term trader who fully understands contango.

What Our Scoring System Says About Energy Stocks

Not all energy stocks are equal. Our 4-pillar scoring system (shareholder returns, growth quality, valuation quality, track record & resilience — 25 points each, 100 total) highlights meaningful differences in quality across the sector.

Here are the top-scoring energy stocks right now:

| Ticker | Name | Score | Yield | P/E | Dividend Years |

|---|---|---|---|---|---|

| TPL | Texas Pacific Land | 80 | 0.31% | 75.1 | 12 |

| MPC | Marathon Petroleum | 73 | 1.76% | 16.4 | 16 |

| OKE | ONEOK | 71 | 4.86% | 15.8 | 42 |

| COP | ConocoPhillips | 68 | 2.80% | 18.4 | 45 |

| FANG | Diamondback Energy | 68 | 2.26% | 31.3 | 8 |

| CTRA | Coterra Energy | 68 | 2.88% | 14.4 | 36 |

| EOG | EOG Resources | 67 | 3.04% | 14.4 | 37 |

A few standouts worth understanding:

MPC — Marathon Petroleum (Score: 73) — Refiners benefit doubly from oil spikes. They buy crude oil and sell gasoline, diesel, and jet fuel. When crude surges, the “crack spread” — the margin between raw oil and refined products — often widens, boosting profits. MPC has a sentiment score of 80 (one of the highest in the sector) and 16 consecutive years of dividends. At a P/E of 16.4, it’s reasonably priced for the earnings it generates.

OKE — ONEOK (Score: 71) — ONEOK is a midstream pipeline company. It doesn’t drill for oil — it moves it. Pipeline fees are typically contracted years in advance, making revenue more predictable than an E&P company’s. The 4.86% yield is the highest among top-scored energy stocks, backed by 42 years of continuous dividend payments. If you want energy exposure without betting directly on oil prices, midstream is the way.

EOG — EOG Resources (Score: 67) — A pure exploration and production company with a reputation for capital discipline and low-cost operations. 37 years of continuous dividends, a P/E of just 14.4, and a 3% yield. When oil prices are high, EOG’s profits surge. When they fall, EOG’s low cost structure means it remains profitable when competitors are bleeding cash.

The surprise: TPL — Texas Pacific Land (Score: 80) — The highest-scoring energy stock isn’t an oil producer at all. TPL owns 880,000 acres of land in the Permian Basin and collects royalties from oil companies that drill on its property. Think of it as a landlord for the energy industry — it benefits from production growth without taking on drilling risk. The score of 80 reflects strong fundamentals, but the P/E of 75 and 0.31% yield mean the market is already pricing in a lot of future growth. High quality, but not cheap.

Notable contrast: XOM and CVX — The two biggest names in energy score just 46 and 51, respectively. Why? Both have high P/E ratios (22.5 and 28.6), and while their dividend track records are legendary (51 and 43 years), their growth and valuation metrics pull the overall scores down. Household names aren’t always the best investments.

The Commodity ETF Cheat Sheet

If you do want commodity ETF exposure — whether for diversification, inflation hedging, or a tactical oil bet — here’s how the main options compare:

| ETF | Tracks | Expense Ratio | Tax Form | Best For |

|---|---|---|---|---|

| XLE | S&P 500 Energy Stocks | 0.09% | 1099 | Core energy equity exposure |

| USO | WTI Crude Futures | 0.60% | K-1 | Short-term oil price trades |

| BNO | Brent Crude Futures | 1.00% | K-1 | Global oil benchmark exposure |

| DBC | Broad Commodity Basket | 0.87% | K-1 | Diversified commodity hedge |

| PDBC | Broad Commodity Basket | 0.59% | 1099 | Tax-friendly commodity hedge |

| GSG | S&P GSCI Commodities | 0.75% | K-1 | Energy-heavy commodity exposure |

The critical distinction: XLE is not a commodity ETF. It holds stocks — actual companies with earnings, dividends, and business operations. It doesn’t suffer from contango. For long-term investors, this matters enormously. XLE gives you oil exposure plus dividends plus business growth. That’s why it’s up 22%+ YTD while pure oil futures ETFs have lagged the spot price despite the crisis spike.

If you want broad commodity exposure in a diversified portfolio, PDBC is the simplest choice — lower expense ratio than DBC, similar performance, and it issues a 1099 instead of a K-1, which means your tax preparer won’t hate you.

The Risks: Why You Shouldn’t FOMO Into Oil

Before you rush to buy anything with “energy” in the name, consider these historical patterns:

Geopolitical spikes reverse fast. The 1990 Gulf War spike? Oil doubled in 3 months, then gave it all back in 6. The 2022 Russia-Ukraine spike to $130? Back under $80 within a year. The pattern is consistent: crisis drives a sharp spike, then supply adjusts, demand drops, and prices normalize. Buying after a 35% weekly surge is historically a losing trade.

The SPR is loaded. The U.S. Strategic Petroleum Reserve holds approximately 415 million barrels — more than half its capacity. The White House says no release is currently planned, but that can change with a single press conference. A surprise SPR release could knock oil prices down 10-15% in days. It happened in 2022 when President Biden released 180 million barrels, and crude dropped from $120 to $80 over the following months.

Demand destruction is real. $90+ oil slows economies. Airlines cut routes. Consumers drive less. Factories scale back. Industrial activity contracts. Every dollar added to a barrel of oil removes demand somewhere in the global economy. High oil prices contain the seeds of their own reversal — it’s one of the most reliable patterns in commodity markets.

OPEC+ has spare capacity. Saudi Arabia alone can ramp production by roughly 2 million barrels per day. If prices stay elevated, the incentive to pump more increases — even among countries that publicly support production cuts. Cheating on OPEC quotas is as old as OPEC itself.

The bottom line: If you didn’t own energy before this week, you already missed the easy money. The best time to buy energy stocks was six months ago when nobody was talking about oil. Chasing a crisis spike is market timing, and most investors get that wrong.

What to Do Instead

Here’s the practical takeaway:

If you already own energy stocks: Hold them. Companies like MPC, OKE, and EOG aren’t one-week trades — they’re businesses with decades of dividend history. The crisis may boost their earnings this quarter, but you bought them (hopefully) for their long-term fundamentals, not for a geopolitical spike.

If you want to add energy exposure: Wait for the dust to settle. Geopolitical premiums don’t last forever. When oil pulls back from crisis highs — and historically it always does — that’s your entry point. Use our scoring system to identify the highest-quality companies, and focus on the ones paying sustainable dividends with reasonable P/E ratios.

If you want commodity diversification: A small allocation to PDBC (5-7.5% of your portfolio) provides inflation hedging without the tax headache. This is a strategic allocation, not a tactical bet — hold it permanently as part of a diversified portfolio.

If you’re tempted to buy USO or BNO: Understand that you’re making a short-term directional bet on oil prices, and that contango will work against you every month you hold. If you’re right about the direction and the timing, you’ll profit. If you’re wrong about either, you’ll lose money — possibly even if oil goes up over the long term. This is a trader’s instrument, not an investor’s.

The Iran crisis is real. The supply disruption is serious. But smart investing means thinking in years, not weeks. The energy sector has always been cyclical — crises come and go, but quality companies keep drilling, refining, and paying dividends through all of it.

Oil prices and ETF data referenced in this article are as of March 6, 2026. This article does not constitute financial advice. All investment decisions are your own. Past performance does not guarantee future results.